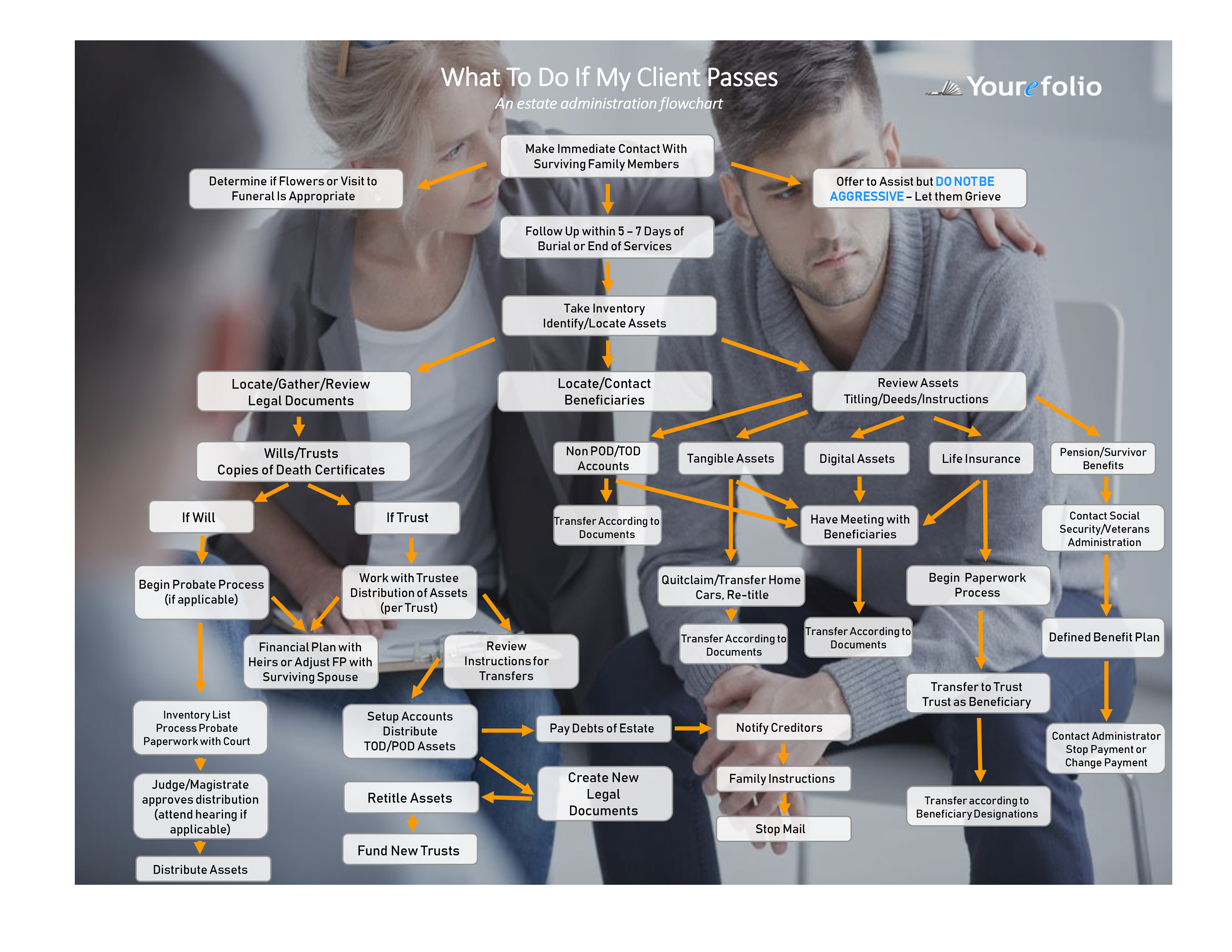

By 2060, almost one in five people living in the United States will be foreign born.

Currently, according to statistics reported by The Atlantic, more than 975,000 international students attend U.S. colleges and universities each year. One third of these students are from China. Many of these students remain in the U.S. after graduation for professional opportunities as well as to begin families of their own.

The continuing influx of non-resident alien children and grandchildren coming to the U.S., coupled with the projected international global wealth transfers, is estimated to reach $16 trillion over the next three decades, which has resulted in an increased trend of international families establishing U.S. trusts.

Do you want to Become a Member to receive latest content from Industry Leaders? YES, TELL ME HOWTrend Towards U.S. Trusts

Recently, international families without relatives in the U.S. have, nonetheless, opted to use the U.S. for their trusts. The combination of modern trust laws, the greater demand for U.S. investments, a desire for political stability and the protection of property, as well as the desire to establish a trust in a non-blacklisted country, have driven this trend. The modern trust laws in the most popular U.S. trust jurisdictions, such as Alaska, Delaware, Nevada, New Hampshire, South Dakota and Wyoming, are attractive to international families as they provide flexibility and control, tax savings, asset protection, privacy (versus secrecy) among other key advantages. While this trend continues to grow, historically, some international families sought U.S. trust situs because they had family in the U.S., typically children or grandchildren. Considering the above statistics, planning for such international families is set to grow in the coming years. To plan for these wealth transfers, advisors are incorporating efficient structures for international families with U.S. beneficiaries that use modern trust laws in the popular modern trust jurisdictions in the United States.

Foreign Grantor Trusts

One of the more popular modern trust options for these families is the foreign grantor trust, or FGT, with a U.S. trustee in a modern U.S. trust jurisdiction. Generally, while the NRA grantor is alive, if there are no U.S. situs assets, then there are no U.S. income, gift and estate taxes. The FGT often will hold shares of a non-U.S. entity holding either foreign and/or U.S. situs property. The non-U.S. entity acts as an estate tax blocker for U.S. situs assets. The non-U.S. entity can also hold U.S. situs assets producing interest income, resulting in the 30 percent withholding taxes or treaty rates being withheld at the entity level. If the non-U.S. entity owned by the FGT holds publicly traded U.S. securities, both federal and state capital gains are generally saved along with U.S. estate taxes, thus making U.S. securities a very attractive investment for NRAs.

NRA Domestic Dynasty Trust

The establishment of an NRA dynasty trust, while the foreign parents or grandparents are alive, provides another option for an international family with U.S. beneficiaries.

If done properly, an NRA citizen parent or grandparent can transfer an unlimited amount of assets onshore into an NRA dynasty trust without any gift, estate or generation-skipping transfer taxes. NRAs aren’t subject to the $11.18 million gift and GST tax exemption limits of a U.S. citizen or green card holder. The unlimited gift exemption generally only applies if NRAs are gifting non-U.S. situs assets, usually cash. Furthermore, assets aren’t subject to state income tax if the trust is established in a no-income tax modern trust jurisdiction. Additionally, the trust can continue forever or for a very long time for the benefit of U.S. beneficiaries by providing asset protection as well as many other trust, privacy and tax benefits.

Standby Domestic Dynasty Trust

The standby or pour-over dynasty trust is a structure often implemented for NRAs with U.S. beneficiaries who’ve established trusts or other planning vehicles in offshore jurisdictions. The standby domestic dynasty trust lessens burdensome income tax filing and reporting requirements for U.S. beneficiaries as well as the negative U.S. income tax rules on distributions of accumulated income after the NRA’s death. On the grantor’s death, the foreign offshore trust “pours over” the offshore trust assets to an existing standby domestic dynasty trust for the benefit of the U.S. beneficiaries. Typically, such trusts are cost-effective and are nominally funded (for example, $10) during the NRA’s lifetime, usually resulting in a one-time set-up fee until fully funded on the pour-over at the NRA’s death, at which point annual trustee fees would apply.

The standby dynasty trust allows for grantors to retain the planning they’ve done in their home country and/or offshore while also having a vehicle in place for their U.S. beneficiaries that offers all the benefits of the NRA domestic non-grantor dynasty trust.

Foreign Trust Change of Situs

Many NRAs with U.S. beneficiaries may not want to wait until their death for their offshore trust to pour over to a standby domestic dynasty trust. Alternatively, they may wish to change the situs of their offshore/foreign trusts to the U.S. while they’re alive. This frequently happens when foreign beneficiaries become U.S. persons. Generally, a foreign trust changes offshore trust situs to the U.S. by using a domestic corporate trustee in one of the modern trust jurisdictions. The domestic trustee (or offshore trustee) declares a new U.S. trust, mentioning the purpose of the new trust as part of the declaration. The foreign trustee then pays over trust assets with a deed of distribution to the new domestic trust. This can also be accomplished via a decant by distributing assets from an old trust into a new trust with new terms, for the benefit of one or more of the beneficiaries of the first trust. It’s important to note that there may be potential tax issues, such as undistributed net income, accumulations distributions and throwback rules, with either method of changing the situs of an offshore foreign trust to the U.S. However, if there are U.S. beneficiaries of a foreign trust that don’t change situs before the death of the foreign grantor or pour over to a U.S. domestic trust at the foreign grantor’s death, the U.S. tax and tax reporting requirements for the U.S. beneficiaries will be extremely burdensome.

The glass continues to be half full regarding international families and NRAs choosing the U.S. as a favored trust situs for their U.S. family. Powerful trust laws, tax savings, asset protection and privacy, as well as solutions to political and regulatory concerns, all combine to make the U.S. their trust situs of choice.

This is an adapted version of the author’s original article in the June 2018 issue of Trusts & Estates.